What Is a 1-0 Buydown Mortgage and How Does It Work in 2026?

A New Orleans Realtor breaks down the no-cost buydown program now available on conventional, FHA, and VA loans

Loan Programs You Should Know About: The No-Cost 1-0 Buydown

A lender I work with just brought this to my attention and I asked enough questions to feel good about sharing it.

It’s called a no-cost 1-0 buydown. Here’s exactly how it works.

For your first 12 months, your mortgage payment is calculated at a rate 1% lower than your actual note rate. In month 13 it adjusts to your permanent rate and stays there for the life of the loan. The cost of that first-year reduction is paid by the investor — not rolled into your rate, not added to your loan balance, not coming out of your pocket at closing.

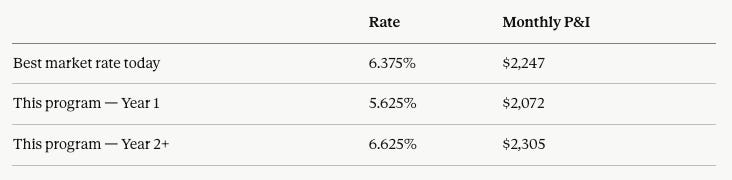

The honest math on a $450,000 purchase (20% down, $360,000 loan):

The tradeoff worth understanding:

This program’s permanent rate is 6.625%, about 0.25% above the most aggressive rate available right now. So you are trading a slightly higher long-term rate for meaningful short-term payment relief. If rates drop enough to refinance before month 13, your blended cost over the first two years still beats most alternatives. If rates don’t move, you’re at 6.625% long term.

Who this actually makes sense for:

A buyer who is cash-constrained at closing and wants breathing room in year 1 while they get settled. Someone furnishing a home, absorbing moving costs, or just wanting a lower payment while they adjust to homeownership. Not the right product for someone who qualifies for the best rate and plans to stay 10+ years without refinancing.

Available on conventional, FHA, and VA all loan terms and LTVs.

The lender behind this program is John Ismail at C2 Financial. As always, shop around and ask your lender how their rate compares before committing to any program.

Questions about buying a house in today’s market?